By Andrew Irumba

As a parliamentary committee started quizzing Bank of Uganda (BoU) top officials on the seven closed banks, TheSpy Uganda has chanced on very incriminating and classified information indicating that former Executive Director in charge of Supervision Ms. Justine Bagyenda, while still at the central bank ordered Dfcu executives to keep Crane Bank’s bad books off the record as away of sweeping their dirt under the carpet since it was after all,DEAL-DONE!

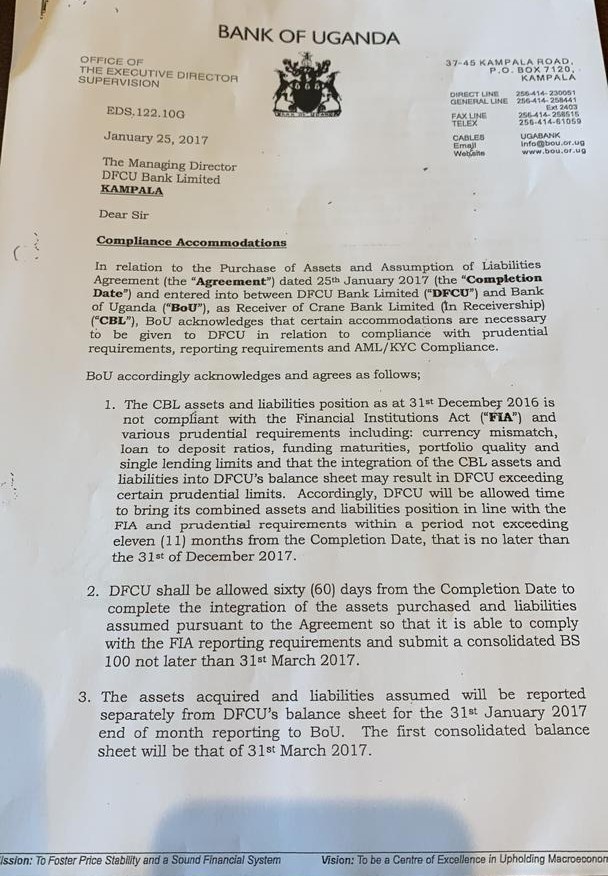

According to a January 25th, 2017 letter already in our armpits, written by Ms.Bagyenda to the Managing Director Dfcu Bank Limited, titled ‘compliance accommodation’, she says that in relation to the purchase of asserts and assumption of liabilities agreement dated January 25, 2017 which was the completion date and entered Dfcu and Bank of Uganda as a receivership of Crane Bank Limited, BoU acknowledged that certain accommodations are necessary to be given to Dfcu in relation to compliance with prudential requirements, reporting requirements and AML/KYC compliance.

“The assets acquired and liabilities assumed would be reported separately from Dfcu’s balance sheet for the 31th January 2017 end of month report to BoU. The first consolidated balance sheet will be that of 31th March 2017. The non- performing loans and advances acquired by Dfcu will be managed and reported on separately from Dfcc’s pre-transaction balance sheet for a period of at least twelve months,” Bagyenda wrote.

The bad books are records indicating details and securities of people that take loans from any lending institution. However, despite Dfcu being given CBL by BoU, it wasn’t mandatory for them keep bad books because they belong to shareholders of CBL.

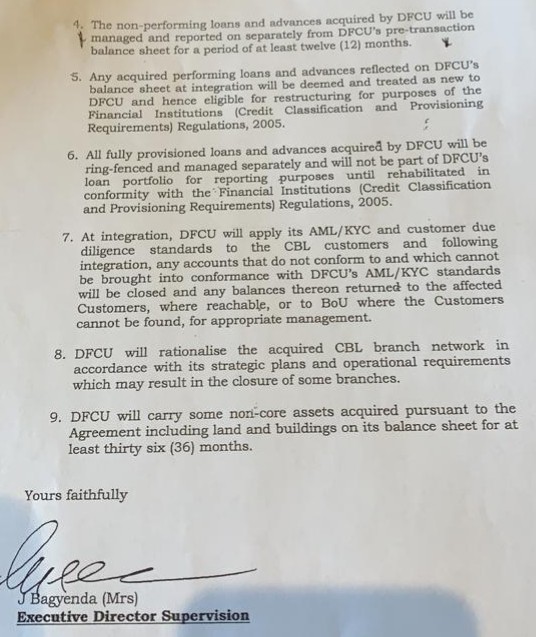

She explained that any acquired performing loans and advances reflected on Dfcu’s balance sheet at integration will be deemed and treated as new to Dfcu and hence eligible for restructuring for purposes of the financial Institutions (credit classification and provisioning requirement. She also directed that all fully provisioned loans and advances acquired by Dfcu will be ring-fenced and managed separately and would not be part of Dfcu’s loan portfolio for reporting purposes until rehabilitated in conformity with the Financial Institution Act.

“At integration, Dfcu will apply its AML/KYC and customer due diligence standards to the CBL customers and following integration, any accounts that do not comform to and which cannot be brought into confomance with Dfcu’s AML/KYC standards will be closed and any balance thereon returned to the affected customers, where reachable, or to BoU where the customers cannot be found for appropriate management” she wrote.

She further emphasized “Dfcu will rationalize the acquired CBL branch network in accordance with its strategic plans and operational requirements which may result in the closure of some branches. Dfcu will carry some non-core assets acquired pursuant to the agreement including land and buildings on its balance sheet for at least 36 months.

According to sources, the said directive was done in connivance between Deputy Governor Louis Kasekende, outgoing Dfcu MD Juma Kisaame Dfcu bank limited board chairman Jimmy Mugerwa and the two conflicted lawyers (David Mpanga of Bowmans and Timothy Masembe of MMASK Advocates).